Perspectives and expectations of financial reports

Understanding financial statements is not just a role reserved for bean counters, CFOs and your casino’s GM. It’s important that anyone who wants a seat at the table, whether today or as their career grows, is confident in understanding these reports.

In two previous articles, we’ve looked at the reports issued in conjunction with the annual financial statement audit. First, the internal control related reports in the article “Properly Safeguarding the Assets of the Casino and Tribe,” and then the audited financial statements themselves in the article “Understanding Key Financial Statements.”

Now we’re ready to go deeper and get more detailed insight on what to look for when reviewing any financial report, whether that is the audited financial statements or the monthly financials produced internally. In the end, you may still not LOVE to review and analyze financial statements the way that I do, but you should have enough confidence to do so, and as a result, have a greater knowledge of the performance of your casino.

There are two things needed to understand financial reports. Neither of them is an accounting degree. They are perspective and expectations.

You have to have something to measure the numbers against to really evaluate whether they are acceptable, good, or “whoa! what went wrong?” Perspective is a benchmark or yardstick to measure by. Several things can give you this perspective. Budgeted amounts can provide perspective. Is the casino over or under budget? Previous months’ or years’ numbers also provide perspective. What is the trend we’re seeing? Is the casino improving or declining? Industry performance standards are another way to gain perspective. Is our casino performing better or worse than the rest of the industry?

Expectations give you something to use to help evaluate the numbers you see. If you know that the casino had a big promotion last month, you would expect to see a boost in revenues. If not, ask questions. If you know that historically March is the casino’s best month of the year, you expect that it will be true in the current year. If the industry average for wages as a percent of revenue is 21%, you expect your casino’s percentage to be close to the same. If its 25%, ask why there is a difference.

You can probably see that perspective and expectations are also linked together. Often, having perspective creates some of our expectations. Now that you have those tools, let’s dive into the basic financials. For this article we’re going to focus on the Income Statement. Everyone’s primary interest is “how much money did we make?”

Income Statement or Statement of Revenues, Expenses, and Changes in Net Position

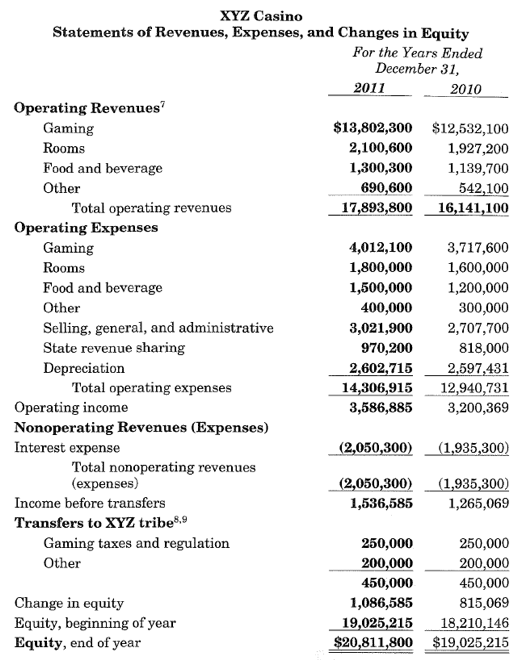

The Income Statement (see example below) gets the most attention because it tells us if the casino is making money. If given an Income Statement with two time periods presented, we can all determine where revenues and expenses may be up or down. However, to truly analyze the performance of the casino, you need more information than is usually provided in audited financials and in many internally prepared financials. There are a few things you can do to analyze performance. (Please note that the percentages below are benchmarks. Actual performance may vary. If the variance is significant, then ask for an explanation).

- As a quick, general operating statistic, you can calculate Operating Income or Earnings Before Interest, Depreciation and Amortization (EBIDA) in some reports as a percentage of total revenue (OI/Revenue). The higher the percentage, the better. We typically see this number between 30% and 40%. This will give you an idea of how efficiently management runs the operation. Of course, we want to look at if it changed much period over period too.

- If revenues and “costs of sales” are presented for various lines of business (LOB), like retail or food & beverage (they are not in the example below), you can calculate their gross profit percentage (revenue less cost of goods / revenue). What percentage is normal will depend on the LOB. For F&B, we like to see 50% or greater. Bar or liquor should be 60% or higher. Retail will vary depending on the products sold, but should be at least 35% to 40%. Tobacco and fuel often have fairly low margins.

- The example below shows revenues and expenses neatly presented by LOB. If you are lucky enough to find this in your financials, you can easily net them together to see how much each line of business contributes to Operating Income. Gaming will likely always have the lion’s share. The thing to watch for are LOBs that contribute little to the Operating Income. Next, you will want to find out if the operating expenses for each LOB include wages and benefits for that LOB. If not, things might not be as rosy as they appear.

- If wages and benefits are shown separately from departmental or general administrative expenses, you can calculate the percent of revenue that this expense represents. If total wages and benefits are more than 30% of overall revenue, your casino is higher than most. If your percentage is significantly different and wages and benefits are presented separately from one another, wages should be in the low 20s as a percent of revenue. Benefits should be in the 6% to 8% range.

- The “Other” or Non-Operating Income (expense) section lists items that are generally beyond the direct control of management, like interest income and expenses. If there is significant interest income, you should see a large amount of investments on the balance sheet. The question for a tribal casino is whether those funds should be held at the casino or transferred to the tribe for them to utilize or invest. If there is a significant amount of interest expense, the footnotes should provide insight into the debt, its terms and any restrictions that may come along with the borrowing.

Statement of Cash Flows

Statement of Cash Flows

I won’t go into a lot of detail about the Statement of Cash Flows, but it is a good companion to the Income Statement. The thing to remember is that the income and expenses on the Income Statement and resulting net income don’t necessarily have a one-to-one relationship with cash. The Statement of Cash Flows will reconcile net income to cash provided or used by the casino. If your property consistently uses more cash than it generates, sooner or later you will have a problem.

Conclusion

With the items discussed above, their behavior over time (expectation) and measurement against benchmarks (perspective) can provide you with valuable information about how the casino is performing. It may show you areas where improved performance could enhance the property’s bottom line. There are a number of ratios and statistics that can provide more insight into the performance of a casino. They are often not provided in audited financial statements unless they include a “Management Discussion and Analysis.” Some internal financial packages also may not provide information, such as coin-in, table drop, hold percentages, win per unit, headcounts, and carded play. We’ll delve more into additional ratios and statistics another time.

Hopefully I haven’t overwhelmed you with information. Always keep in mind that anyone can look at a financial report and gain knowledge when viewed through the lenses of perspective and expectations. You don’t need an accounting degree but knowing a good accountant doesn’t hurt.