A deeper look at your balance sheet

In Part I of “Understanding Casino Financial Statements,” we discussed that two things are needed to understand financial reports, perspective and expectations. You have to have something to measure the numbers against to really evaluate what they are telling you. Then we started building some perspective by looking at the most popular financial statement, the income statement. Now let’s look at the Balance Sheet, or Statement of Net Position. It may not be as exciting as looking to see how much money our property made, but it has a lot of useful information.

Balance Sheet or Statement of Net Position

A few general things to keep in mind about the Balance Sheet or Statement of Net Position (see sample below). First, it is as of a point in time (e.g., at 9/30/XX). Second, its primary purpose is to show us what the casino OWNS and what they OWE. Hopefully, the statement will present at least two years’ information so that we can have some perspective. With these things in mind, let’s go through the statement and talk about what you will likely see.

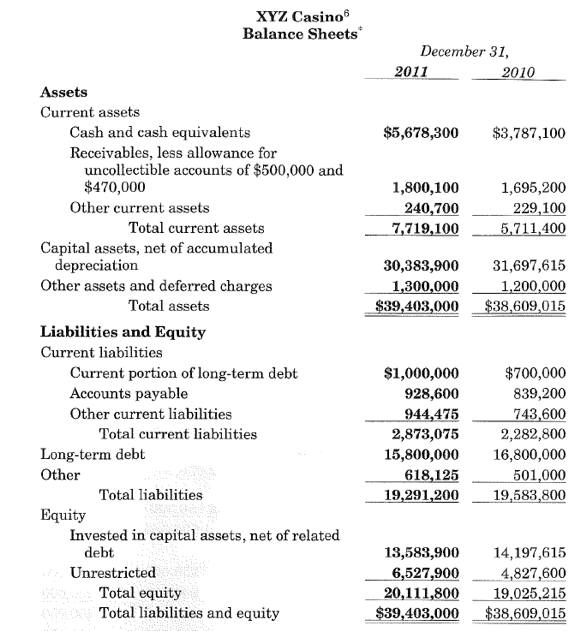

Example Casino Balance Sheet – Understanding Financial Statements by Kevin Huddleston

The thing we like to own most is always first, Cash.

It might say “Cash and Cash Equivalents.” This includes the money in the bank and money in the casino’s vault. The footnotes to the audited financial statements will likely tell us how much is in each category. Internally prepared monthly or quarterly financials may break it out in the statement itself. For the average person, all they can really do is look at the balance in relation to the prior year or months. There are many factors that may cause changes in the cash balances from period to period. Understanding how the casino processes payroll and payables, when debt payments might be due, and how distributions to the Tribe are handled can help you make sense of any fluctuations in cash. Cash in the vault shouldn’t change a lot unless there are changes in the number and types of games offered. The casino should have what is called a “bankroll calculation” that helps determine how much money should be kept in the vault. The gaming commission is supposed to have reviewed and approved the calculation methods.

Accounts Receivable (AR) is usually the next thing listed.

Unless your property extends credit to guests, AR for a casino is comprised primarily of amounts due from credit card, check and ATM processors. These payments are usually collected within a few days. Fluctuations are not uncommon, depending on how the end of the period falls in relation to weekends or holidays. If you have concerns about growing balances, ask for an aging so you can see if there are items that aren’t being collected in a timely manner.

Receivables from the Tribe or other related entities may be listed next.

These can be tricky. Such receivables may or may not be repaid, at least not in a timely manner. You may need to ask how these amounts are handled.

Prepaid Assets may be a line item.

This represents a portion of amounts paid for things that will benefit the casino over the next year. Insurance coverage, equipment maintenance agreements or software support agreements are likely items included here. The balance will be impacted significantly in the month that these items are first paid.

Fixed Assets is often the largest amount shown in the asset section.

Things included here are items purchased above a specific dollar amount that will be used by the property for more than a year. Fixed assets are things like buildings, slot machines, furniture and equipment.

Accounts Payable (AP) is often the first liability listed.

AP represents what the casino owes for goods and services for which they have been invoiced. The balance of AP can fluctuate from period end to period end depending on the casino’s normal payment cycle and whether or not the balance includes any large quarterly or annual payments due. As with AR, if you are concerned about a growing balance in AP, ask for an aging. Not paying bills in a timely manner can indicate issues with performance or cash flow that need to be addressed.

Next, let’s look at accrued liabilities and gaming liabilities.

Accrued liabilities are amounts the casino knows they owe, but have not been invoiced for. This line item may also include payroll-related liabilities, like time worked but not yet paid at period end and the amount of leave time earned.

Gaming liabilities are amounts owed for in-house progressive jackpots, players club points, and chip float. Significant changes in the balance from period to period should be questioned. Another thing to consider here is the amount of liability for retired progressives. Retired progressives can be added to active progressives or utilized for promotions designed to “return” those funds back to the players.

Debt is usually presented as at least two items, long-term and current portion.

It may be all the same debt, but the amount of it due in the next 12 months is presented as the current portion. Long-term is anything due in more than year. If you see increases in this area, in total, obviously there was additional borrowing. It may have been directly related to the purchase of some fixed assets. If the current portion increases significantly, you may want to look at the total current portion in relation to the amount of cash and the amount of income the casino generates in a year to see if there is any cause for alarm or at least a need for some cash flow planning.

The last section will vary.

Depending on whether we are examining a balance sheet or a statement of net position. On the balance sheet you will see equity. For the statement of net position, it is net position. Both are the difference between your assets and liabilities. Both itemize the same basic items.

- First, “Invested in Capital Assets Net of Related Debt” shows whether the casino has equity or net position tied up in fixed assets.

- The other amount shown in this section is “unrestricted” equity or net position. It is possible that this amount may be negative, which may indicate that the casino has a large debt load, is losing money, or money has been distributed to the Tribe or its other enterprises in excess of the amount the casino earned.

A Final Note on this Financial Statement

Footnotes to the audited financial statements should provide you with more detailed information about the individual line items. In fact, the footnotes may provide answers to some of the questions we’ve discussed previously.